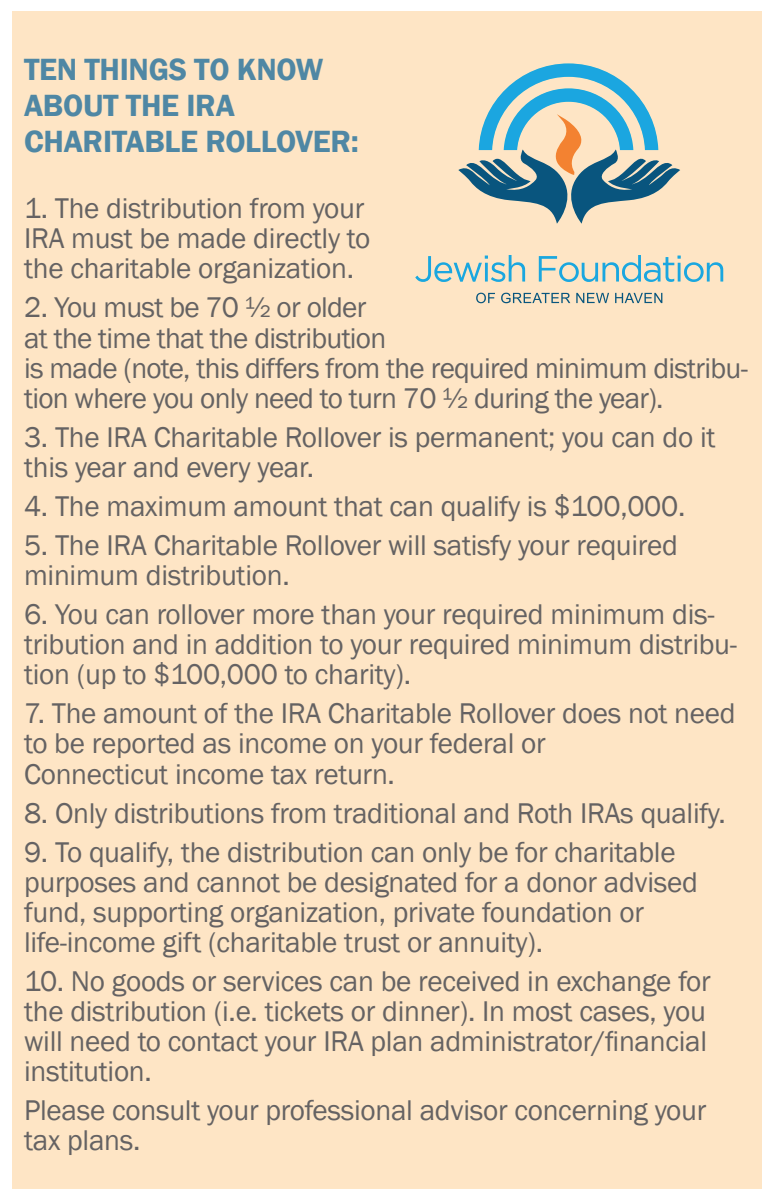

The IRA Charitable Rollover creates an opportunity for donors to establish an endowment or make an outright charitable gift to a charitable organization. Your rollover can be directed for a capital campaign gift, current needs, or restricted for endowment purposes. Your gift can be earmarked for your synagogue, a local Jewish agency, Jewish education, or any program or organization that is important to you.

EXAMPLE: Mr. Cohn distributes $18,000 from his IRA to his synagogue and/or to establish an endowment fund for his synagogue (Mr. Cohn names the fund after his grandchildren).

WITHOUT THE IRA CHARITABLE ROLLOVER: Mr. Cohn would be subject to federal and Connecticut income tax on the amount of the distribution (even if it went straight to charity) -- although he could claim a charitable income tax deduction on his federal return for the donation, he would not be able to do that on a Connecticut income tax return and would have Connecticut income tax liability for the distribution—even if it was given directly to charity.

WITH THE IRA CHARITABLE ROLLOVER: The $18,000 distribution is not taxable income for federal and Connecticut income tax purposes (even if it is being used toward his required minimum distribution)—it is tax neutral. Mr. Cohn has created a wonderful Jewish legacy for his family and community, reduced his Connecticut income tax liability, and reduced his taxable estate!

WHAT IS THE ADVANTAGE? If you already have enough income and your IRA minimum distribution requirement only increases your tax liability, this allows you to donate your distribution directly to charity without realizing federal or Connecticut income tax liability on the amount of the distribution (you will not have to pay Connecticut or Federal income tax on that amount). In addition, if you have a taxable estate, your IRA, will be subject to income and estate taxes (once both spouses are deceased and the IRA is left to your children, grandchildren or other individuals). In fact, in a taxable estate, your non-spouse beneficiaries could end up with 25 cents on the dollar for your IRA assets! The rollover allows you to remove some of those taxplagued assets from your estate while also providing you with the opportunity to make a significant charitable gift. In addition, if you have a secondary smaller IRA, which is not a necessary income source, this is an opportunity to donate that IRA to our community and make a significant and much needed impact. Contact Jewish Foundation of Greater New Haven Executive Director Lisa Stanger at [email protected].

0Comments

Add CommentPlease login to leave a comment